The difference between full, simplified, and modified VAT invoices

In the UK, there are 3 different types of VAT invoices you can send to your clients: full invoices, simplified invoices and modified invoices. Each type has a specific purpose and is used in different circumstances.

If you’re a VAT registered business in the UK, it’s important to understand the difference between the different types of VAT invoices and issue the correct type.

What is a full VAT invoice?

A full invoice is the standard form of invoice used when the sale is subject to VAT. If you’re a VAT registered business that sells taxable products or services, you’ll need to issue a VAT invoice. A full invoice is the most common form, so when in doubt, use this format.

A full invoice must include the following details:

Your business name and address

Your customer’s name and address

The invoice date and date of supply

Your company’s VAT number

A description of the products being sold

The price of each product (exclusive of VAT)

The VAT rate of each product

The quantity of each product

The total amount of the invoice (exclusive of VAT)

The total amount of VAT

You’re required to issue a VAT invoice if any of the products being sold are subject to VAT, but if all of the products are zero-rated, a VAT invoice is not required.

What is a simplified VAT invoice?

A simplified invoice is exactly what you would expect - a simplified version of a full invoice. It includes less information than normal, and, rather than spelling out the total amount due without VAT and how much VAT has been added, it simply tells the customer how much is due, VAT included.

A simplified invoice includes most of the same information as a full invoice, excluding the date, the customer’s details, subtotal, total VAT amount and the price and quantity of each item. It’s a very basic invoice version to show the total amount to be paid by the customer.

Simplified invoices can only be issued for purchases up to £250. If a customer asks for a VAT invoice for sales over this amount, a modified or full invoice must be issued.

What is a modified VAT invoice?

A modified invoice is similar to a full invoice, but it also includes the VAT inclusive price of products and the total amount including VAT.

Modified invoices are only issued for sales exceeding £250 that include taxable products. This type of VAT invoice must be agreed upon with your client to allow VAT inclusive amounts.

A modified invoice will include all of the information that’s found on a full invoice, but the product prices and total amounts will be inclusive of VAT.

Which invoice format should I use?

The invoice format you use depends on the price of the sale and what you and your client have agreed upon. You’ll likely use a full invoice for the majority of your sales.

Full invoices can be used for any amount. Simplified invoices can be used for amounts up to £250. Modified invoices can be used on amounts greater than £250.

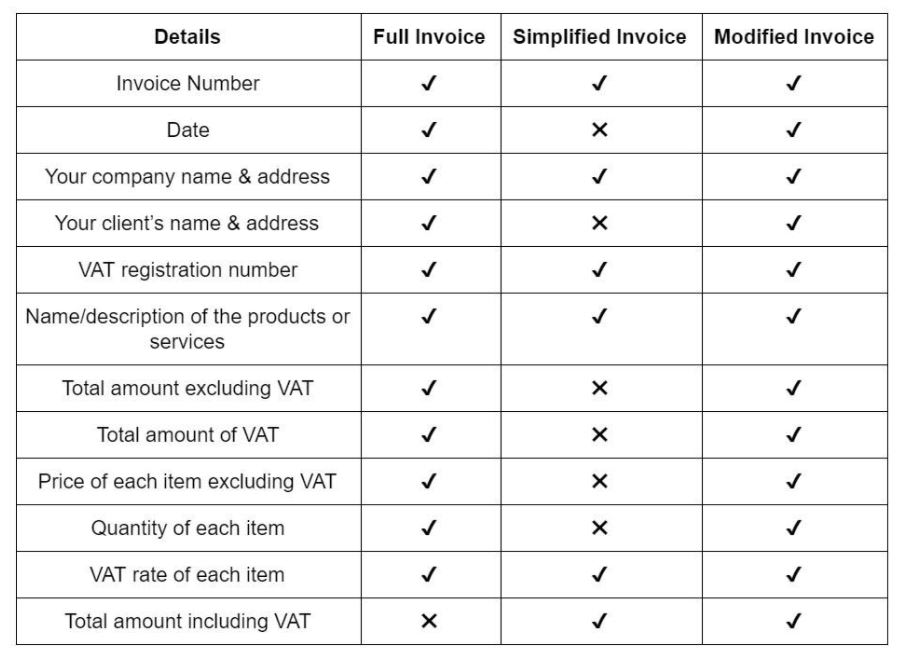

Below, we’ve provided a chart showing the differences between each type of VAT invoice:

Create VAT invoices with invoicing software

You can quickly and easily create and send invoices to clients using invoicing software, like SumUp Invoices. The software ensures that you have all of the required details filled in before you send the invoice to your customer.

If your business is VAT registered, you can enable VAT in your invoicing settings. Then, you can start creating professional VAT invoices in under 1 minute.

If you sell products or services with different VAT rates, you can easily manage this with SumUp Invoices. For each product line you add, you can enter a different VAT rate, and the VAT amounts will be calculated automatically after the subtotal.